[Tren urbano]Proyecto de Inversión Privada en el Tren Ligero de Seúl para mejorar el transporte de las áreas vulnerables del tren urbano.

Background to Light-Rail Projects Driven by Private Investment

In the early 1990s, South Korea’s infrastructure (such as roads, railways, ports and airports) was insufficient to its needs. In the 1980s, the Korean government cut spending in the stated interest of encouraging private development and restructuring of the Korean economy, resulting in lackluster investment in social overhead capital. In the 1990s, distribution costs contrast with GDP was increased and it caused serious traffic congestion around several large areas, including Seoul. The government believed there was a limit to providing funds for construction of infrastructure and that it was important to attract the private sector. In August 1994, it began promoting projects driven by private investment with establishment of the Promotion of Private Capital into Social Overhead Capital Investment Act. However, private investment became more difficult after the financial crisis in late 1997. As a means to stimulate the economy after the financial turmoil, the Act on Private Participation in Infrastructure was completely revised to promote private investment projects through various government policies, and the MRG (Minimum Revenue Guarantee) system is one example of the typical government support measures.

The Seoul city government believes that expansion of the public transit network (primarily of the subway system) is necessary even after the completion of 1st and 2nd subway construction and has explored solutions for poorly-serviced areas. The city promoted a multi-nucleic urban structure and balanced development by strengthening the connection between central regions, and supported development of station influence areas to cope with the demands of eastern and western Metropolitan areas. In particular, the need for additional subway track has emerged due to heavy congestion: 30,000 to 40,000 people per hour use the system especially the 25km section from Gimpo Airport to Banpo and the 16km section from Gayang to Banpo. The Asian financial crisis in 1997, however, made it more difficult for the national and local governments to pay for such needed expansion. In 2003, urban railway debt accounted for 81% of Seoul’s total debt. The operating deficits of the Seoul Metropolitan Subway Corporation and the Seoul Metropolitan Rapid Transit Corporation have mounted, postponing new subway construction. In response to this problem, Seoul attracted private investment to Seoul Metro Line 9 as a private project that includes the MRG. Due to inaccurate estimation of demand, however, the government's share of the funding increased and reduced the MRG system in 2003. In 2006, the system was abolished in private offering projects, and in 2009 for government-set fixed projects.

Recently, Seoul announced plans for major improvements to still-existing poorly-serviced areas despite the continued expansion of the subway line network. According to analysis conducted in 2014, approximately 38% of Seoul is considered poorly-serviced area, with extensive distribution of the rail lines in the city’s northeast, northwest, and southwest regions, causing regional disparity. To address this, and in consideration of requirements for building railway public transport systems, Seoul provided a Railroad Private Project Standard Concession Agreement (proposal). The key details of the improvement measures are to introduce light rail service to poorly-serviced areas and remedy short comings of the financial support on private projects with MRG.

Main Details of Privately-Invested Light Rail Projects

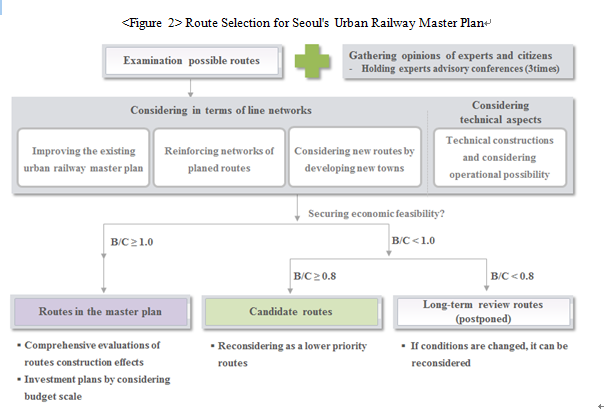

Review of Urban Railway Routes & Route Selection Process (Seoul's Ten-year Urban Railway Master Plan, 2013)

The 10-Year Urban Railway Master Plan aims at balanced growth and focuses on measures to better serve areas of the city with insufficient rail connection, and was drawn up after an environmental impact and sustainability assessment, consultation with relevant agencies and holding several public hearings to listen to residents. The city also reviewed comprehensive feasibility and route evaluations of both routes outlined in the Master Plan and possible routes in the future. Following is the procedure for selection of the routes outlined in the Urban Railway Master Plan 2013.

1) Selection of target routes for review

A total of 37 routes (the existing 8 urban railway master plans and 29 new routes proposed for review) were selected as target routes for review; some were proposed in the 2008 Urban Railway Master Plan and some have been proposed by local governments and citizen.

2) Selection & evaluation of alternative routes for each target route

Detailed alternative routes are selected for review, with connection between routes, urban spatial structure, land use, social/economy/geographic situations, and the existing urban railway network are all considered. That is, the plan determines whether alternative routes will fit into an economic structure through connection with other relevant plans and transportation infrastructure of the surrounding areas, while ensuring services to isolated areas. The following details are reviewed for each alternative route:

○ Possibilities for route expansion, stopovers, depot locations, linking with existing urban railways

○ Operating plans (vehicles, formation, and headway train interval) review

○ Technical details of regional physical conditions and physical obstructions to the route

3) Route selection of route candidates of the master plan

After reviewing alternative routes, existing routes where technical construction is impossible and routes where demand is deemed to be insignificant due to redundancy are eliminated from the primary candidate list.

4) Routes selected for Master Plan

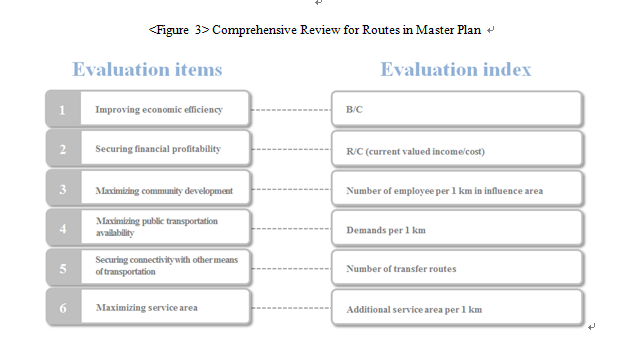

Demand analysis, project cost calculations, and economic feasibility analyses are done for Master Plan candidate routes. Economically feasible routes are chosen and other routes classified as “optimum alternative candidates”, subsequent (candidate) routes and routes for long-term review. A comprehensive review is then begun on indirect effects of route composition.

5) Analysis of master plan routes

The following details are analyzed in accordance with the Urban Railway Master Plan Establishment Guidelines for routes selected for the Master Plan:

○ Transportation demand, changes in the public transit modal share, analysis of main road traffic impact

○ Establishment of construction and operational plans, linked transportation systems, measures to handle road traffic in construction areas

○ Economic / financial feasibility analyses, financial funding measures, annual investment plans

○ Pre-environmental review and pre-disaster impact review

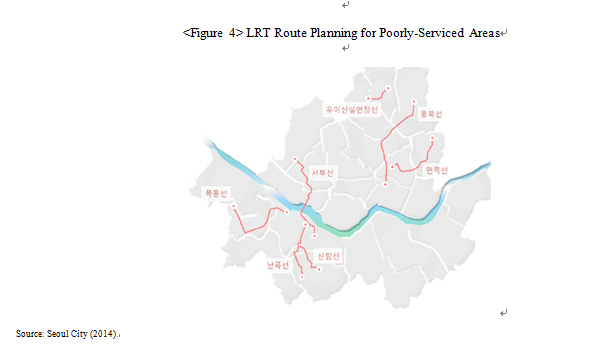

Introduction of Light-Rail Service to Poorly-Serviced Areas

To push forward with plans to increase access to rail for poorly-serviced areas, Seoul may create light rail branches (designed to handle 10,000 passengers/km per day) from existing routes instead of the more costly and time-consuming heavy rail tracks. As a result of comparison with routes for review, poorly-serviced areas can be reached by additional construction in UI new extension line, the northeast line, the Myeonmok line for the northeast region, the west line for the northwestern region, the Mokdong line, the Shillim line, and the Nangok line in the southwest region according to Seoul's (2014) report. The routes were, in fact, selected in the 2008 Urban Railway Master Plan, when they were classified as optimal alternative routes, and there was ongoing demand for construction from residents in poorly-serviced areas. Seoul's light-rail proposal will strengthen integration with the existing urban railway and the Master Plan routes, and includes measures to expand to areas generating massive demand. With these measures, accessibility to urban railway service in poorly-serviced areas will be enhanced, while bus routes will be adjusted to facilitate better connection to the rail system in areas where the proposed light-rail stations will not be within a 10-minute walk.

Additional Financial Support for Existing Private Investment Projects

If Seoul promotes private investment for its light-rail project, various problems are likely, such as operating loss compensation due to excessive demand, and demands are mounting that the project should be financed by the government. On the other hand, state-supported projects often face delays due to budget restrictions. In addition, debate on priority for each route is likely regarding construction period.

To find a middle ground, Seoul is attracting private investment and strengthening government management of the light-rail projects, including a proposal for consistent standards of process for all projects through a Privately-Funded Railroad Project Standard Concession Agreement of Seoul City. The proposed standard ensures a smooth agreement implementation with private businesses by providing agreement-related organizations and professional manpower throughout the time of agreement, construction and operation. With this, Seoul City was able to secure private funds, including a sound capital structure of which the city can modify agreement details, such as the profit return rate in case of changes in the financial market henceforth.

The supplement of the rate system in the existing private business procedures

The Seoul’s2008 Urban Railway Master Plan allows pricing differences. Since private firms that conduct private projects cannot collect huge project expenses, the plan is to allow higher pricing than the current basic transportation rate to help private businesses recover their investment. However, this met with opposition from residents in poorly-serviced areas, so the city decided to follow the existing public transit fare system in Seoul (basic rate, transfer discounts). However, the difference of the rate offered by private businesses and the basic rate is supported by Seoul City, with the scale of support based on actual demand. The amount of financial aid for the northeast line over the last 15 years is expected to be 177.4 billion won. However, under the MRG standard, the cost would have been around 314.6 billion won, which may help Seoul City's finance.

xpectancy effects according to Seoul City's light-railway expansion

Effect on Transportation

With light-rail expansion of the subway system, Seoul expects increased public transit modal share and improvement to subway accessibility. The designed light-rail routes will be constructed in poorly-serviced regions, and upon completion, all residents of Seoul will be able to reach a subway station within 10 minutes. Moreover, it is expected that areas with easy subway access (within a 500m radius of subway stations) will increase to 72% from the current 62%, which will reduce average travel time for residents in these light-rail serviced areas by 20%, and by 9% for all residents of Seoul. Lastly, the plan is expected to improve the public transit modal share, while decreasing passenger car modal share and reducing the costs of traffic congestion in the city by 1.2 trillion won annually (as of 2011, total annual traffic congestion costs are approximately 8 trillion won).

Socio-economic Effects

It is difficult in the planning stage to predict the socio-economic effects of Seoul's light-rail projects driven by private investment. However, we can estimate the future effect of Seoul's Light-railway project driven by private investment through urban railway and traffic infrastructure system composition that had been implemented for several years. Urban railway and transport infrastructure projects led by private investment have so far been favorable for private operating agencies, leading to a rise in government financial support and also wasting taxpayers' money. Despite these disadvantages, such projects do tend to begin operations on time, thereby enhancing operational efficiency. From a socio-economic viewpoint, the effect of private investment on Seoul's urban railway and transportation infrastructures are classified into three types:

Growth effect owing to private investment

A large amount of private funds were injected into urban railway and transportation infrastructure, allowing the city to do more in other areas with its own limited financial resources. Since the 1997 Asian financial crisis, private investment projects, promoted as part of an economic stimulus package during the economic recession, have contributed to a booming economy.

Transportation convenience at an earlier stage

With construction of Seoul Metro Line 9, transportation convenience has materialized at an earlier stage, resulting in a return of 1.45 trillion won or 19.4% of the total project expenses. Similarly,14 recent private road projects initiated by Seoul City would have been dramatically delayed if they had been solely dependent on public financing.

Revitalization of regional economies & financial effects

Seoul Metro Line 9 also created additional effects - remigration of the market economy around stations. With the opening of Metro Line 9, accessibility to Gangseo and Yeouido has dramatically improved, where a department store connected to the Express Business Terminal Station (line No. 9) saw their weekend sales up 26.7% year-on-year, up 19.2% compared to the previous weekend, and 9.7% more visitors. Business at restaurants and convenience stores in Metro Line 9 stations has also doubled, resulting in significant revenue.

Limitations & Need for Improvement

While private investment offers many advantages to the construction of transportation infrastructure (including urban railway projects) such as funding and provision of timely services, there are also disadvantages. Seoul City has experienced many trials and errors in promoting various private projects. One notable problem involving a privately-funded project has been with Seoul Metro Line 9, whose operating entity was offered a Minimum Revenue Guarantee as part of the plans to boost access in Gangseo district to public transit. However, due to the incorrect estimation of demand, the city had problems paying the operating subsidy to Seoul Metro Line 9 management agency as it had become more substantial then expected and increase of fare as the agency had the right to decide fare. If actual revenues fall short of projections stated in the concession agreement, Seoul Metro Line 9 was guaranteed to receive 90% of the minimum operating revenue (the MRG) for up to 5 years from commencement of operations, 80% from 2006 to 2010, and 70% from 2011 to 2015 regardless of actual operational revenue.

The MRG program has been abolished now, and based on failed private-investment projects such as Seoul Metro Line 9, project procedures have been reviewed to ensure the city does not bind itself into unreasonable payments when promoting light-rail projects to private investors. However, the private investment project is also addressed with improvements and limitations. While the fare subsidy had been supported due to accurate estimates in the past, the demand is now estimated based on actual demand, which reduced funding amount of Seoul. However, light-rail construction projects are very likely to require more funding from the city, which already has debts from its existing public transit systems. This means that plans for future light-rail projects need to have sufficient measures to ensure sustainability.

| Total | 2009 | 2010 | 2011 | |

|

MRG (100 million won)

|

838

|

131

|

293

|

414

|

Provision of a management system for private project flexibility

In order to minimize Seoul's financial burden arising from private investment-driven light-rail projects and to ensure sustainability, the city needs to implement flexible plans for effective management and periodical conditions. The light-railway project in schedule may change due to financial realities for the city, including social and economic conditions. Seoul needs to accommodate the needs of subway construction and provide a systematic measure that reflects a variety of fluctuations for activate participation of private investment.