Restructuración del Esquema de Seguridad Básico de Seúl Correspondiente a la Reforma de la Seguridad de Subsistencia Básica Nacional

Summary

There is a need to relax the Seoul Basic Security Scheme’s beneficiary selection criteria and adjust its allowance payment method to avoid income reversal among the beneficiaries.

1. Introduction

The Seoul Basic Security Scheme must be restructured in response to the National Basic Livelihood Security System reform

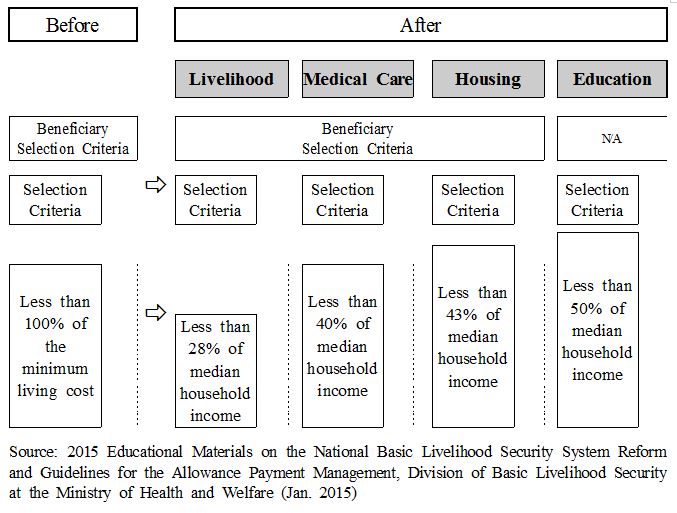

The national government of Korea has been endeavoring to better support the livelihood of low-income individuals. In this regard, it has introduced a system called the National Basic Livelihood Security System (NBLSS) in 2000. The system provides financial support to the poor whose earnings are less than minimum cost of living. Later in July 2015, the government has undertaken the system reform. In the process, two significant changes have been made: First, the national government has expanded the scope of beneficiaries (refer to <Figure 1>). Second, it has adjusted the allowance payment method (refer to<Figure 2>). Previously, the beneficiaries of NBLSS were selected based on one criterion – that is, whether their income can cover minimum cost of living. Once they were accepted, they all received the same amount of allowance. After the reform, the national government now determines who receives the allowance by weighing multiple factors. Instead of taking only livelihood into account, it looks at other areas of needs such as medical care, housing and education. In other words, it pays a wider range of people with varied financial needs. Still NBLSS does not attend to everyone in pecuniary difficulties. This is why the Seoul Basic Security Scheme (SBSS) has been implemented. It supplements income of the poor who are ineligible for NBLSS, yet greatly suffer from poverty. In this sense, two systems are closely related to one another.

<Figure 1> NBLSS Beneficiaries before and after the Reform

.JPG)

<Figure 2> Beneficiary Selection Criteria and Allowance Payment Scheme of NBLSS before and after the Reform

As a result of the NBLSS reform, a slightly greater number of Seoul citizens are now NBLSS beneficiaries. SBSS should accordingly adjust the scope of its beneficiaries and how it secures their livelihoods.

2. Main Findings

This research is comprised of three parts in large. In the beginning, it explains what changes the NBLSS reform has brought to its beneficiaries. Next, it delineates how the reform has affected Seoul citizens. In conclusion, it proposes various options for how to improve the beneficiary selection criteria and living allowance payment scheme of the SBSS.

SBSS ought to change in response to the NBLSS reform. In particular, its beneficiary selection criteria need to be adjusted to better find a blind spot where the poor are being neglected. This report urges the Seoul Metropolitan Government (SMG) to improve the system in the following two directions.

SBSS ought to change in response to the NBLSS reform. In particular, its beneficiary selection criteria need to be adjusted to better find a blind spot where the poor are being neglected. This report urges the Seoul Metropolitan Government (SMG) to improve the system in the following two directions.

Following the directions of changes suggested earlier in this report, the SMG should (1) ease the beneficiary eligibility requirements, (2) adjust the baseline beneficiary household income to represent the exact median Seoul household income, and (3) relax the optional criteria. This study has drawn 13 options for system adjustment in three aforesaid areas of change (refer to <Table 2>). It has been discovered that the selection rate increases by applying each adjustment. More people will receive the benefit provided by the SBSS when each adjustment is applied to the system.

Following the directions of changes suggested earlier in this report, the SMG should (1) ease the beneficiary eligibility requirements, (2) adjust the baseline beneficiary household income to represent the exact median Seoul household income, and (3) relax the optional criteria. This study has drawn 13 options for system adjustment in three aforesaid areas of change (refer to <Table 2>). It has been discovered that the selection rate increases by applying each adjustment. More people will receive the benefit provided by the SBSS when each adjustment is applied to the system.

<Table 2> Options for Beneficiary Selection Criteria Adjustment

From various combinations of 13 options, we propose herewith the final draft for the adjustment of the SBSS beneficiary selection criteria (refer to <Table 3>). It suggests easing the income requirement that the beneficiaries must comply with. It also recommends increasing the baseline value of financial assets from 10 million to 15 million Won. Another significant change proposed here is the removal of beneficiary requirement regarding car ownership.

From various combinations of 13 options, we propose herewith the final draft for the adjustment of the SBSS beneficiary selection criteria (refer to <Table 3>). It suggests easing the income requirement that the beneficiaries must comply with. It also recommends increasing the baseline value of financial assets from 10 million to 15 million Won. Another significant change proposed here is the removal of beneficiary requirement regarding car ownership.

Not every eligible beneficiary family lives in Seoul. Therefore, it is inappropriate for the SBSS to have the median Seoul household income as the baseline value for its income requirement. Yet taking out such a requirement would not be understood nor accepted by most Koreans. Experts argue that this also poses a problem: The beneficiaries of the SBSS would receive a larger amount of allowances than the relatively poorer beneficiaries of the NBLSS. Many would certainly argue that this is unfair.

In regards to the optional criteria, this report proposes raising the baseline value of financial asset requirement. In addition, we believe in the feasibility of removing beneficiary requirement related to car ownership: Most of ineligible beneficiaries do not own cars. Even they do, their cars are not worth much.

<Table 3> Final Draft for the Adjustment of SBSS Beneficiary Selection Criteria

On the assumption that the SMG adopts the adjustments proposed in this study, 3,633 families would be added to the pool of the SBSS beneficiaries each year from 2012 to 2014 (calculated by applying the change to the number of households declined by the NBLSS during the same period).

On the assumption that the SMG adopts the adjustments proposed in this study, 3,633 families would be added to the pool of the SBSS beneficiaries each year from 2012 to 2014 (calculated by applying the change to the number of households declined by the NBLSS during the same period).

However, this number is susceptible to change given that the size of annual NBLSS applicant pool fluctuates. It may also be affected by the national government that is aggressively encouraging eligible beneficiaries to apply for new system at the moment.

<Table 4> Estimated Size of SBSS Beneficiary Pool with the Adjusted Beneficiary Selection Criteria

<Figure 3> Income Reversal among Beneficiaries across the Income Brackets

.JPG)

Reformed NBLSS would embrace extra 30.7 percent of non-beneficiary households in Seoul

This study has utilized the data from the welfare-related database managed by the national government. It has applied the new extended beneficiary selection criteria of reformed NBLSS. The result shows that maximum 30.7 percent of Seoul citizens who were previously found ineligible for NBLSS would now be accepted according to new criteria : 22.1 percent comes from people who qualify for livelihood assistance; the rest 8.6 percent is represented by new recipients of medical care and housing support.

NBLSS declined the application of 15,175 families each year from 2012 to 2014. If those applicants all reside in Seoul, 4,569 of them would be embraced by the system in accordance with its new beneficiary selection criteria.

NBLSS declined the application of 15,175 families each year from 2012 to 2014. If those applicants all reside in Seoul, 4,569 of them would be embraced by the system in accordance with its new beneficiary selection criteria.

<Table 1> Estimated Number of Extra Households Approved by New NBLSS (accumulated no.)

(Unit : %, No. of households)

| Category | Livelihood | Medical care | Housing | Education |

| Baseline Income | 30% of median income | 40% of median income | 43% of median income | 50% of median income |

| Beneficiary Selection Rate | 22.1 | 28.1 | 30.7 | 52.5 |

| No. of extra households approved by NBLSS | 3,354 | 4,264 | 4,659 | Paid Individually |

Seoul needs to relax the SBSS’s beneficiary selection criteria so that it can better fulfill its initial purpose and help a greater number of Seoul citizens in need

SBSS ought to change in response to the NBLSS reform. In particular, its beneficiary selection criteria need to be adjusted to better find a blind spot where the poor are being neglected. This report urges the Seoul Metropolitan Government (SMG) to improve the system in the following two directions.First, remove inappropriate elements from the current beneficiary selection criteria. This would raise the beneficiary selection rate, meaning the system can help more citizens in financial hardship. At the moment, the SBSS requires its beneficiaries to qualify for all six criteria – if one wishes to receive the allowance, he or she must satisfy a set of requirements for income, asset, financial asset and car ownership categories. Moreover, their caregivers such as family members who have a legal responsibility to support them also need to meet income and asset requirements. This multi-dimensional criteria certainly reduce the chance of people getting accepted by the system. There lies another problem. That is, the requirements related to car ownership and financial asset overlap.

Second, serve the fundamental purpose of the SBSS. SMG has designed and installed the system in pursuit of addressing the problem with the NBLSS: It applies utterly tight criteria to legal caregivers of its beneficiaries. Further, it pays the equal amount of living allowance to all the beneficiaries across the country. In other words, the system fails to recognize that price level in each region varies. Consequently, some impoverished people end up being neglected in blind zones. This is basically why the SMG has created the SBSS in the first place: To help the poor neglected by the NBLSS. The national government should concentrate on serving this very purpose.

Second, serve the fundamental purpose of the SBSS. SMG has designed and installed the system in pursuit of addressing the problem with the NBLSS: It applies utterly tight criteria to legal caregivers of its beneficiaries. Further, it pays the equal amount of living allowance to all the beneficiaries across the country. In other words, the system fails to recognize that price level in each region varies. Consequently, some impoverished people end up being neglected in blind zones. This is basically why the SMG has created the SBSS in the first place: To help the poor neglected by the NBLSS. The national government should concentrate on serving this very purpose.

This study suggests options for system adjustment in three areas: beneficiary eligibility requirements, baseline beneficiary household income, and optional criteria

Following the directions of changes suggested earlier in this report, the SMG should (1) ease the beneficiary eligibility requirements, (2) adjust the baseline beneficiary household income to represent the exact median Seoul household income, and (3) relax the optional criteria. This study has drawn 13 options for system adjustment in three aforesaid areas of change (refer to <Table 2>). It has been discovered that the selection rate increases by applying each adjustment. More people will receive the benefit provided by the SBSS when each adjustment is applied to the system.<Table 2> Options for Beneficiary Selection Criteria Adjustment

(Unit: %)

| Area of adjustment | Baseline | Supporting data | Beneficiary selection rate change | |

| Current criteria | 28.6 | |||

| ① Ease the beneficiary eligibility requirements | ①-1 | Median income of two-person households in Seoul | Modified only the minimum living cost in the current equation | 31.2 |

| ①-2 | Median income of three-person households in Seoul | Used a median Seoul household income | 32.8 | |

| ①-3 | No baseline | Serves the basic purpose of SBSS | 38.4 | |

| ② Adjust the baseline beneficiary household income | ②-1 | 40% of median Seoul household income | The minimum living cost(now)≒40% of median income | 35.7 |

| ②-2 | 45% of median Seoul household income | Used a figure between Options 1 and 3 | 38.4 | |

| ②-3 | 50% of median Seoul household income | Applied the concept of relative poverty | 40.5 | |

| ③ Relax the optional criteria | ③-1 | Financial assets worth 15 million Won | Based on the median value of financial assets owned by Seoul citizens (source : Field Study of Welfare Conditions in Seoul 2013) | 30.9 |

| ③-2 | No requirement for car ownership | Both car ownership rate of beneficiaries and the prices of their cars are low | 33.9 | |

| ③-3 | No requirement for financial assets | Financial assets are already counted in assets | 38.3 | |

| ③-4 | No requirements for car ownership and financial assets | Solves the problem with the current multi-dimensional criteria | 44.6 | |

Raise the baseline value of financial assets to 15 million Won and eliminate the beneficiary requirement related to car ownership

From various combinations of 13 options, we propose herewith the final draft for the adjustment of the SBSS beneficiary selection criteria (refer to <Table 3>). It suggests easing the income requirement that the beneficiaries must comply with. It also recommends increasing the baseline value of financial assets from 10 million to 15 million Won. Another significant change proposed here is the removal of beneficiary requirement regarding car ownership.Not every eligible beneficiary family lives in Seoul. Therefore, it is inappropriate for the SBSS to have the median Seoul household income as the baseline value for its income requirement. Yet taking out such a requirement would not be understood nor accepted by most Koreans. Experts argue that this also poses a problem: The beneficiaries of the SBSS would receive a larger amount of allowances than the relatively poorer beneficiaries of the NBLSS. Many would certainly argue that this is unfair.

In regards to the optional criteria, this report proposes raising the baseline value of financial asset requirement. In addition, we believe in the feasibility of removing beneficiary requirement related to car ownership: Most of ineligible beneficiaries do not own cars. Even they do, their cars are not worth much.

<Table 3> Final Draft for the Adjustment of SBSS Beneficiary Selection Criteria

| Category | Current | New | |

| Beneficiary households without family assistance | Income | 100% of the minimum living cost | 40% of the median household income |

| Asset | 100 million won | No change | |

| Financial asset | 10 million won | 15 million won | |

| Car | Declined if a household owns a car | Remove this requirement | |

| Beneficiary households with family assistance | Income | The minimum living cost of two-person household | 40% of the median three-person household income(no change in calculation) |

| Asset | 500 million won | No change | |

With the adjusted beneficiary selection criteria, 3,633 families would be newly chosen as the SBSS beneficiaries each year

On the assumption that the SMG adopts the adjustments proposed in this study, 3,633 families would be added to the pool of the SBSS beneficiaries each year from 2012 to 2014 (calculated by applying the change to the number of households declined by the NBLSS during the same period).However, this number is susceptible to change given that the size of annual NBLSS applicant pool fluctuates. It may also be affected by the national government that is aggressively encouraging eligible beneficiaries to apply for new system at the moment.

<Table 4> Estimated Size of SBSS Beneficiary Pool with the Adjusted Beneficiary Selection Criteria

(Unit: %, No. of households)

| Estimate | Note | |

| Beneficiary selection rate | 33.3 | |

| No. of eligible beneficiary households | 10,911 | 15,175 households × 71.9%1) |

| No. of accepted beneficiary households | 3,633 | 10,911 × 33.3% |

| 1) The rate of previously declined applicants turning into the recipients of livelihood or medical care assistance is excluded | ||

SBSS has three different amounts of living allowance to pay its beneficiaries in each of three income brackets. This method needs to be adjusted

NBLSS reduces the amount of allowance it pays to its beneficiaries when their earnings rise. In the case of the SBSS, it has three income brackets. The system pays its beneficiaries the equal amount of allowance according to which bracket they belong to. This means that even if a beneficiary earns a greater income than others in the same income bracket, he or she can still receive the same amount as long as they stay in the same bracket. Thus, they may find the current scheme beneficial. However, it embodies a problem: A beneficiary receiving the most in the first income bracket may end up having greater earnings than the one receiving the least in the second income bracket (refer to <Figure 3>). This is called “income reversal.”

<Figure 3> Income Reversal among Beneficiaries across the Income Brackets

Option 1: Devise more income brackets. SMG can more easily determine the amount of allowance and better prevent income reversal

One way to make the SBSS more effective is to devise more income brackets – five, seven or ten as shown in <Figure 4>. This is to be done while maintaining the system’s basic framework designed by the SMG. This option can contain confusion to the minimum level. Moreover, it may ease the process of deciding the amount of allowance. With more brackets, income reversal can better be prevented. Yet income reversal cannot be completely unraveled as long as the SBSS sets the income bracket as a basis to determine the amount of allowance payable to its beneficiaries.

One way to make the SBSS more effective is to devise more income brackets – five, seven or ten as shown in <Figure 4>. This is to be done while maintaining the system’s basic framework designed by the SMG. This option can contain confusion to the minimum level. Moreover, it may ease the process of deciding the amount of allowance. With more brackets, income reversal can better be prevented. Yet income reversal cannot be completely unraveled as long as the SBSS sets the income bracket as a basis to determine the amount of allowance payable to its beneficiaries. <Figure 4> Five-Stage Income Brackets

.JPG)

Option 2: Take out the earnings of beneficiary households from the maximum amount of allowance, and then pay them the leftover

Alternatively, the SBSS may pay its beneficiary households what is left in the maximum amount of allowance after deducting their earnings. This option can prevent income reversal. But the problem is that a beneficiary might end up receiving none. It is because the SBSS limits the maximum allowance up to a half of how much the NBLSS pays to its beneficiaries. To deal with such a problem, the system may impose a fixed minimum amount for the allowance. However this poses another problem: The maximum 67.9 percent of the beneficiaries might end up receiving the same minimum allowance. This makes the whole purpose of dividing the beneficiary pool into different income groups meaningless.

Alternatively, the SBSS may pay its beneficiary households what is left in the maximum amount of allowance after deducting their earnings. This option can prevent income reversal. But the problem is that a beneficiary might end up receiving none. It is because the SBSS limits the maximum allowance up to a half of how much the NBLSS pays to its beneficiaries. To deal with such a problem, the system may impose a fixed minimum amount for the allowance. However this poses another problem: The maximum 67.9 percent of the beneficiaries might end up receiving the same minimum allowance. This makes the whole purpose of dividing the beneficiary pool into different income groups meaningless.<Figure 5> Paying 50% of Living Allowance

.JPG)

Option 3: Adjust the amount of allowance payable to beneficiary households according to change in their earnings

The last option is to apply a linear equation(i.e. Y = aX + b demonstrated in <Figure 6>), so that the amount of allowance payable to a beneficiary decreases by a certain rate according to an increase in their incomes. Since the allowance changes accordingly as a beneficiary’s earnings change, income reversal can be avoided. Furthermore, it prevents the problem found with Option 2: a concentrated number of beneficiary households receiving the minimum allowance. The key to the success of this option is to determine the correct value of ‘a’(i.e. the rate of allowance reduction). Such a task, however, is difficult in that the value has to be calculated every year for the amount of living allowance changes every year.

The last option is to apply a linear equation(i.e. Y = aX + b demonstrated in <Figure 6>), so that the amount of allowance payable to a beneficiary decreases by a certain rate according to an increase in their incomes. Since the allowance changes accordingly as a beneficiary’s earnings change, income reversal can be avoided. Furthermore, it prevents the problem found with Option 2: a concentrated number of beneficiary households receiving the minimum allowance. The key to the success of this option is to determine the correct value of ‘a’(i.e. the rate of allowance reduction). Such a task, however, is difficult in that the value has to be calculated every year for the amount of living allowance changes every year.<Figure 6> Graded Payment Method Proportionate to the Income of Beneficiary

Option 3 is a sensible and logical choice compared to the other two alternatives

Of all three options proposed in this report, Option 3 would be the best choice. Yet this option (as well as the other two) would inevitably result in paying less to some beneficiaries under the current payment scheme of the SBSS – which limits the amount of maximum allowance to 50 percent of the NBLSS allowance. This is unavoidable as the system would have to pay less to the beneficiaries who currently receive more, vice versa, in order to avoid income reversal. This problem may continue until society fully adapts to new method. To tackle such a matter, the SMG may compensate beneficiaries who receive a less allowance than before 2015 by paying them the amount taken out from their previous allowance. Or it may alter the present eligibility requirement for the maximum allowance payment.

Of all three options proposed in this report, Option 3 would be the best choice. Yet this option (as well as the other two) would inevitably result in paying less to some beneficiaries under the current payment scheme of the SBSS – which limits the amount of maximum allowance to 50 percent of the NBLSS allowance. This is unavoidable as the system would have to pay less to the beneficiaries who currently receive more, vice versa, in order to avoid income reversal. This problem may continue until society fully adapts to new method. To tackle such a matter, the SMG may compensate beneficiaries who receive a less allowance than before 2015 by paying them the amount taken out from their previous allowance. Or it may alter the present eligibility requirement for the maximum allowance payment.<Table 5> Advantages and Disadvantages of each Method

| Method | Advantages | Disadvantages |

| Devise more income brackets and set a different allowance amount for each bracket | ∙ Better prevent income reversal ∙ Require a smaller budget than now ∙ Make it easier to determine the allowance amount |

∙ Not fully prevent income reversal ∙ Result in some beneficiaries receiving less allowance than now |

| Set the 50% of maximum amount of allowance as a cap | ∙ Avoid income reversal ∙ Require the smallest budget among other methods |

∙ Hurts the system’s effectiveness as it pays many beneficiaries the same allowance set for a lower limit ∙ The total amount of allowance payable to beneficiaries is smaller than other options ∙ Result in some beneficiaries receiving less allowance than now |

| Set the 100% of maximum amount of allowance as a cap | ∙ Best serves the purpose of guaranteeing a basic standard of living ∙ Avoid income reversal |

∙ May conflict with the NBLSS living allowance ∙ Require a relatively larger budget |

| Pay a varied amount of allowance according to a beneficiary’s earnings | ∙ Avoid income reversal ∙ Prevent beneficiaries concentrating in a lower limit ∙ Require a moderate size of budget |

∙ Coefficient value must be recalculated every year ∙ Result in some beneficiaries receiving less allowance than now |

3. Conclusions & Policy Recommendations

Various options are anchored in the analysis of numerous data. Yet imperfect features have been found in the data. Besides multiple factors that are not visible in the data affect the beneficiary selection process in reality. In this regard, we strongly suggest that the SMG draw a final plan for the SBSS improvement by weighing every relevant factors. It should also utilize every available information and skills in the process – the result of data analysis, information on the actual progress of system improvement and practical judgment.

Carefully decide the boundary of the SBSS by factoring in its close relationship with the NBLSS

When the SBSS was being first designed, the NBLSS then had a fixed amount of allowance. Thus, it was not complicated to select its beneficiaries. But now, it has a different amount set for each assistance category. In response, numerous experts have raised questions about who should be added to the pool of the SBSS beneficiaries. Some argue that the system must embrace every family that is ineligible for the NBLSS. Their argument rests on that the system should focus on serving its fundamental purpose: protecting the livelihood of Seoul citizens. Others contend that the SBSS should not accept households receiving any other kinds of government assistance.

When the SBSS was being first designed, the NBLSS then had a fixed amount of allowance. Thus, it was not complicated to select its beneficiaries. But now, it has a different amount set for each assistance category. In response, numerous experts have raised questions about who should be added to the pool of the SBSS beneficiaries. Some argue that the system must embrace every family that is ineligible for the NBLSS. Their argument rests on that the system should focus on serving its fundamental purpose: protecting the livelihood of Seoul citizens. Others contend that the SBSS should not accept households receiving any other kinds of government assistance.There are some issues with the allowance amount and the way the SBSS pays it. The system must ensure that its beneficiaries are selected based on fair criteria. It needs to make sure that no doubts or questions about the validity or fairness of beneficiary selection process are raised by either beneficiaries of NBLSS or SBSS. If the SBSS accepts too many people for its beneficiaries, it will conflict with the NBLSS. If it embraces too little, on the other hand, it will fail to help people maintain a basic standard of living.

『Welfare Standards of Seoul Citizens』, which is the declaration on welfare for Seoul citizens, rules that any citizen of Seoul should be guaranteed a basic standard of living. Thus, the SBSS should pay its beneficiaries more than 50 percent of the NBLSS allowance – the NBLSS pays 70 percent of the minimum living cost. Yet one must question whether it is really appropriate to support the poor by increasing the cash payment through the SBSS. Securing a basic standard of living falls under the responsibility of the national government. If SMG provides greater financial support, confusion about the role of the national and local governments may arise. This may widen the gap between Seoul and other municipalities in the country.